When climate and our economy collide, the impact is everyone’s problem. The solution requires bold, decisive, and collective action – in an ever-evolving landscape.

Businesses are transforming operations and making big commitments. While new carbon, biodiversity, and clean energy projects are driving innovation.

And when the whole world is in a state of transformation, it is difficult to keep up with the pace of change.

But change doesn't have to be complex.

CORE Markets gives businesses the tools to demystify clean energy and carbon markets, and take decisive action to net zero.

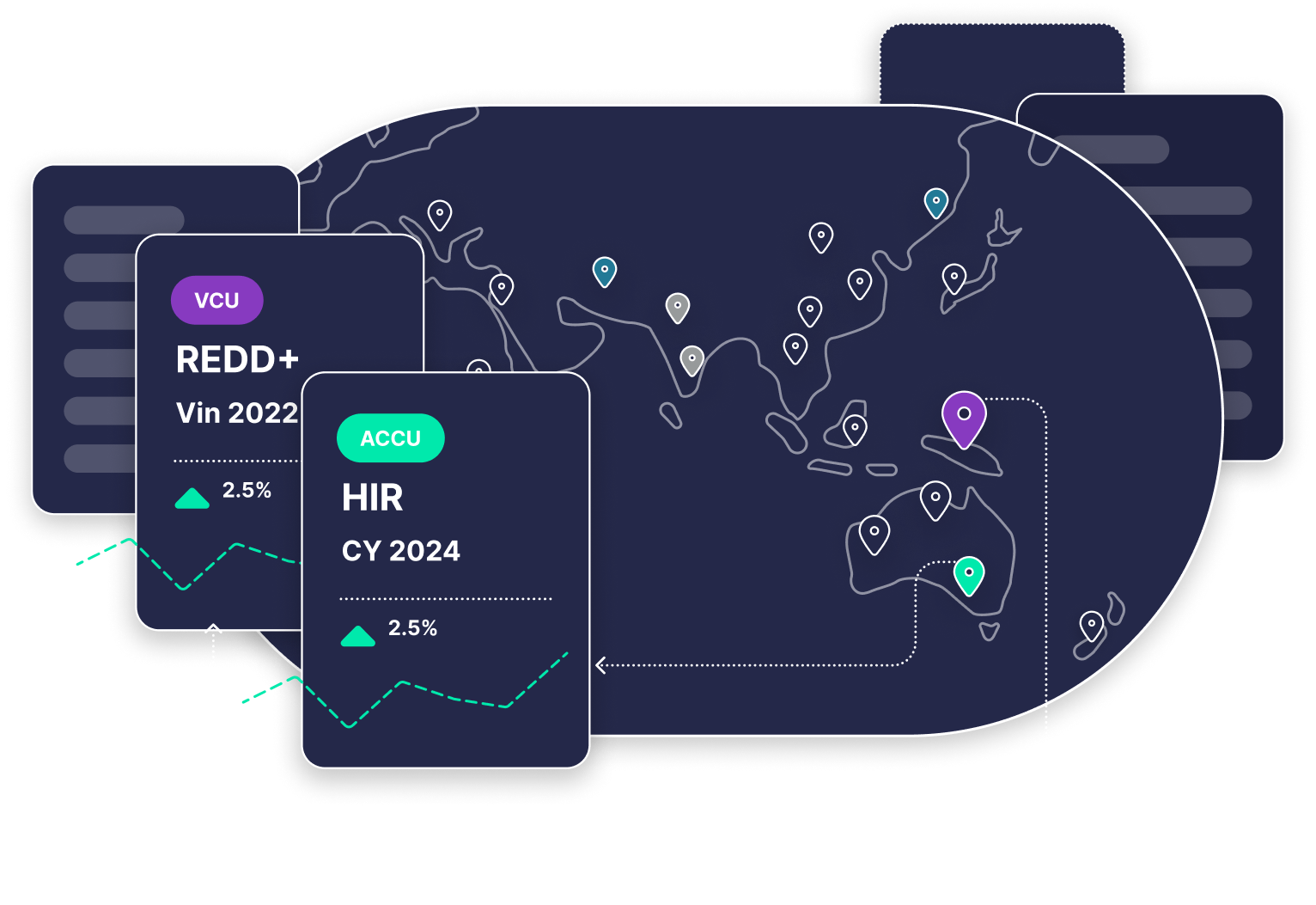

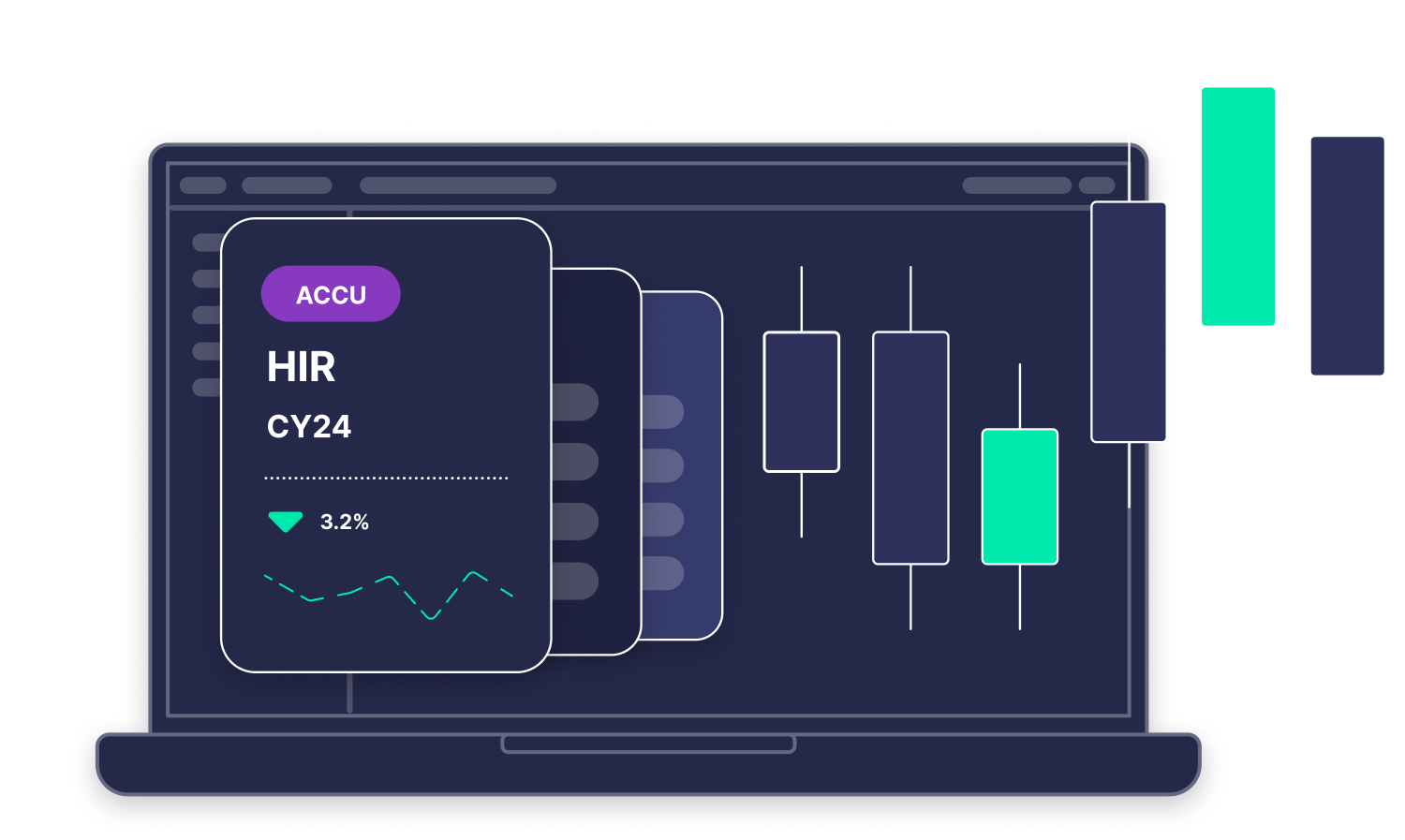

The CORE Markets platform connects sustainability teams, wholesale market participants and project developers with live carbon and clean energy markets.

CORE Markets acknowledges Aboriginal and Torres Strait Islander Peoples as the Traditional Custodians of the land on which we live and work, and acknowledges and pays respect to their Elders, past, present and emerging.